I'm meaning this in the nicest way possible. Please, no sarcastic comments, etc. Does anyone know exactly what the current Prosper policies or procedures are regarding late loans?

As I understand it, once a loan goes <15 late, Prosper follows up with the borrower. When the loan goes late (+30 days), Prosper transfers the loan to the collection agency that then tries to collect on the loan. I think this part I understand.

What I don't understand, is when a loan is transferred back from the collection agency to the in-house "post charge-off collection" bucket.

I have loans that are 6-7 months overdue and are still at Penncro. I have other loans of similar age that are in no state that the Prosper interface can tell me what they are in - thus I assume they are in the Post Charge-off Collections bucket.

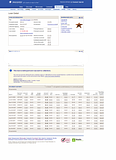

Then I have this loan (click for larger view):

The borrower stopped paying regularly in December of 2007. However, (s)he has made additional payments in March, May June and July.

On the payments in March, May and June, I got late fees. On the payment in July, I didn't get late fees, but the collection agency still took their slice.

My best explanation is that since there were only a few days between the June and July payments, there were no additional late fees calculated and thus the borrower got to pay off some regular interest and principal. Without having run the numbers, I'd actually have to wonder if the borrower didn't have accumulated interest to pay off though.

Thanks for any clarification.

PS. I didn't ask Prosper CS since they still haven't responded to my previous question regarding my loans in BK status. I'm not in a mood to waste more time jumping though the hoops to send them email just to not get a response.